It was another busy week jampacked with key economic data and updated company earnings.

Monday kicked off on a cautious note as weaker than expected growth data from China hit risk appetite. In the commodity space, Brent marched into new week less than 2% away from its highest price back in October 2018. The dollar struggled for direction while gold waited for a fresh catalyst. In other news, Apple unveiled the new MacBook Pro models at a major Mac event.

With third-quarter earnings season in full swing, our trade of the week was none other than the S&P500. We questioned whether earnings would propel the index to record highs this week. Well, on Thursday the S&P500 touched a new record high with another record hit on Friday before comments from Federal Jerome Powell triggered a slight pullback.

Interestingly, the mood across markets improved on Tuesday as solid corporate earnings soothed concerns around inflationary pressures. As risk-on market mood returned, the dollar index (DXY) weakened to a one-month low while gold bugs drew strength from a weaker dollar and lower Treasury yields.

In our mid-week technical outlook, it was all about the dollar. As strong corporate earnings rekindled risk appetite, investors departed from safe-haven destinations like the dollar to riskier assets. In fact, the greenback depreciated against every single G10 currency for the week with the DXY wobbling above 93.50.

As the dollar weakened, this provided fresh trading opportunities on various currency pairs. Taking a look at the USDJPY, prices seem to be experiencing a pullback with 112.80 acting as the first point of interest. A breakdown below this point could encourage a decline towards 112.00.

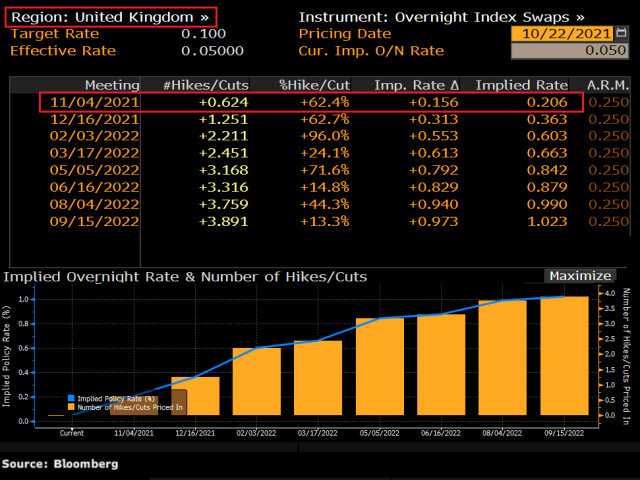

On the data front, UK CPI figures came in weaker than expected on Wednesday, with a 0.3% month-on-month rise in September, against expectations of a 0.4% gain, pushing the year-on-year rate of inflation down to 2.9% from 3% in August. Despite the mildly disappointing inflation data, markets are still pricing in a good chance of a first BoE rate hike at the November MPC meeting.

A wave of risk aversion swept across financial markets on Thursday as fresh concerns over Chinese property developer Evergrande left investors on edge. The company reported that the planned sale of its property services arm had collapsed which increased the risk of default. However, on Friday there were reports that Evergrande remitted $83.5 million to a trustee account at Citibank which was a welcome development to markets. Nevertheless, this does not change the fact that the property developer still has $300 billion in liabilities.

Refocusing back on commodities, it was a positive week for gold despite the choppy price action witnessed over the past few days. Price pushed above the 50-day Simple Moving Average mid-week with comments from Jerome Powell on Friday regarding tapering and interest rate hikes triggering explosive levels of volatility. Despite gold spiking as high as $1813.66, the precious metal concluded the week closing below the psychological $1800 level.

Oil also had a positive week, finding comfort near multi-year highs. WTI Crude has appreciated a whooping 72%+ since the start of 2021 while Brent is not too far behind, gaining roughly 65%. Persistent strength in prices also means pressure on OPEC+ to increase output is growing. The US and India have already asked the cartel to pump more, but the group is wary of additional non-OPEC+ supply growth next year. The next OPEC+ meeting is scheduled for November 4.

Brent bulls have the October 2018 high in their sights and may hit this checkpoint before the month concludes.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.